Insurance still matters in 2026, but its weak points are harder to hide. Buyers want protection, yet rising costs, harder claims, dense policy terms, and trust issues keep getting in the way. For firms tracking insurance in Uganda and the wider East Africa market, that matters. Growth is fragile when customers feel covered on paper but exposed in real life.

Higher costs are making insurance harder to justify

Insurance feels expensive because the costs behind it keep climbing. Medical care, car repairs, imported parts, and weather-related losses all push prices up. Fraud adds pressure too, so insurers protect margins by charging more.

Premiums keep rising while household and business budgets stay tight

Inflation hits insurance from many sides at once. Clinics charge more, repairs cost more, and floods create bigger losses. That pressure lands in the premium. Coverage that once felt manageable now competes with rent, school fees, fuel, and payroll. In Uganda, debate around high medical bills and health insurance shows why buyers are feeling squeezed.

Many people still pay for cover they may never use

That creates a value problem. Insurance works best when a serious loss happens rarely, but customers don't always feel that benefit. After years of paying, a small payout can feel like pouring water into sand. The protection exists, yet the value can feel distant.

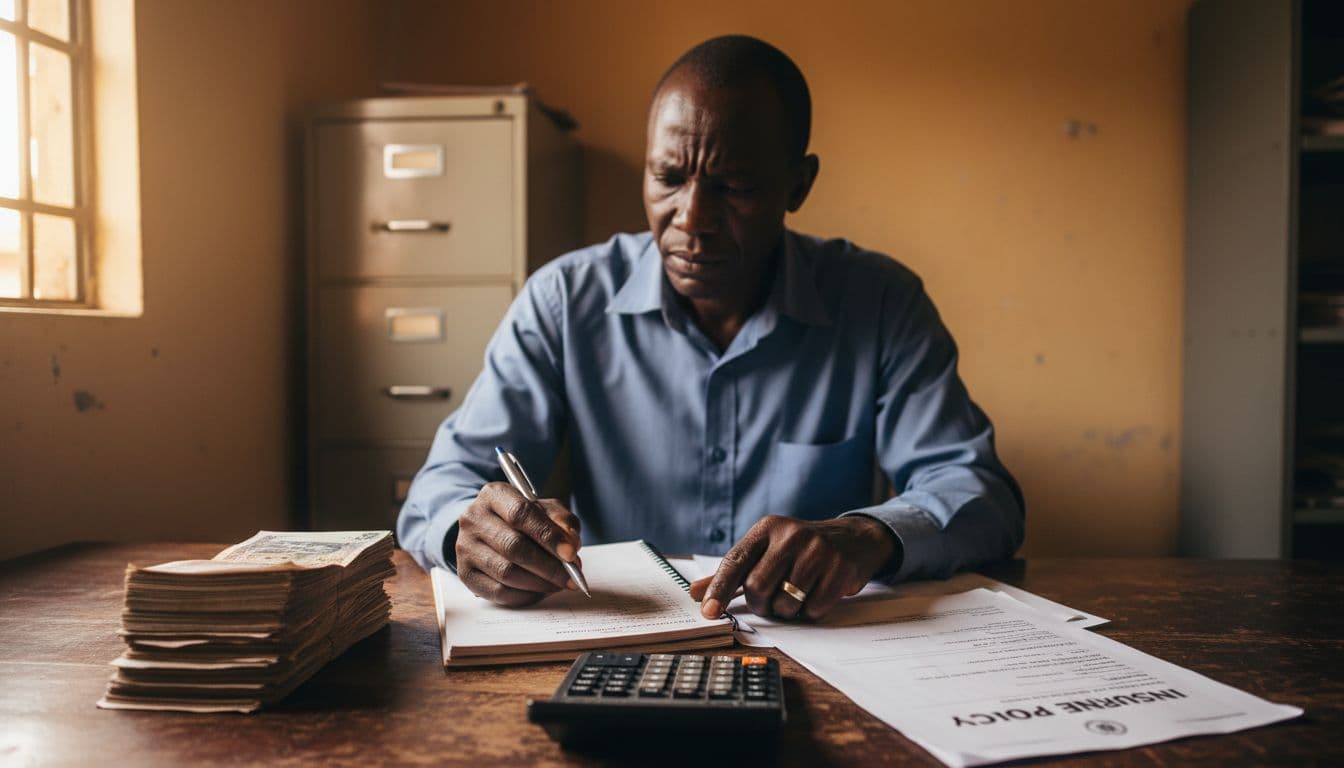

Policy terms and claims processes can still frustrate customers

Price gets attention, but complexity often does more damage. Customers remember the claim they thought was simple, then learned it wasn't.

Fine print, exclusions, and waiting periods can cause costly surprises

Many disadvantages come from what a policy does not cover. Excesses, caps, waiting periods, and exclusions can shrink a claim fast. A health plan may exclude some conditions. A property policy may limit flood damage. When wording is hard to follow, buyers hear "protected" at sale time and "not included" later.

Slow claims and heavy paperwork damage confidence

Delays make everything worse. Clients may submit forms, receipts, photos, and police letters, then wait weeks for updates. Poor communication turns review into suspicion. In insurance in Uganda and nearby markets, digital tools are improving, but many customers still face paper-heavy processes and uneven service quality.

Insurance can leave gaps that matter more in 2026

Even when people buy cover, important risks may still sit outside the fence.

Some risks are hard to insure well, especially new and climate-related risks

Cyber loss, floods, drought, and business interruption are tough examples. Some policies limit these risks, charge much more for them, or avoid them completely. That leaves businesses exposed where they most need help.

Low awareness and limited trust keep many people underinsured

Confusion also blocks uptake. Past bad experiences and low financial literacy push people toward the cheapest policy, or none at all. Work on microinsurance challenges in Uganda shows that trust and understanding still shape demand across underserved markets.

The biggest disadvantages of insurance in 2026 are clear, cost, complexity, delays, and coverage gaps. Insurance still has an important role, but weak product design erodes trust fast. Clearer wording, better-fit cover, and faster claims would go a long way toward fixing that.

إرسال تعليق